Should You Refinance If Rates Drop by 1%?

A one-percentage-point mortgage rate drop can create real monthly savings, but refinancing only makes sense if the savings outweigh closing costs, term reset risk, and your plans for the home.

A common refinance rule of thumb says that you should consider refinancing when mortgage rates drop by at least 1%. That can be a useful starting point, but it is not enough to make the decision.

A rate that is one percentage point lower can reduce your monthly principal and interest payment. It may also lower the total interest you pay over time. But refinancing usually comes with closing costs, a new loan term, possible points, appraisal or title fees, and the risk of restarting the mortgage clock.

The better question is not simply, “Did rates drop by 1%?” The better question is: Will the refinance improve your financial position over the time you expect to keep the home?

Key Takeaways

- A 1 percentage point rate drop can be meaningful. On a larger loan balance, the monthly savings can be hundreds of dollars.

- The refinance has to beat the costs. Closing costs, points, lender fees, title fees, appraisal fees, and prepaid items can reduce or erase the benefit.

- Your break-even point matters. If you sell or refinance again before the break-even point, the refinance may not have enough time to pay for itself.

- Do not compare only the monthly payment. A new 30-year loan can lower the payment while keeping you in debt longer.

- The right answer depends on your goal. Lower payment, shorter loan term, removing mortgage insurance, cash-out, and payment stability are different refinance goals.

First: 1% Usually Means One Percentage Point

When people say rates dropped by 1%, they usually mean one percentage point. For example, a mortgage rate dropping from 7.00% to 6.00% is a one-percentage-point drop.

That is different from a 1% relative decrease. A 1% relative decrease from 7.00% would only lower the rate to about 6.93%, which would not change the payment very much.

For refinance decisions, most homeowners are thinking about a full percentage-point move, such as 7.25% to 6.25%, 6.75% to 5.75%, or 6.50% to 5.50%.

How Much Could a 1 Percentage Point Drop Save?

The savings depend mostly on your remaining loan balance, current rate, new rate, and new loan term. The bigger the loan balance, the more a lower rate can change the monthly payment.

Here is a simple example using a new 30-year fixed refinance from 7.00% to 6.00%. This example looks only at principal and interest, not property taxes, homeowners insurance, HOA dues, mortgage insurance, or closing costs.

| Loan Balance | Payment at 7.00% | Payment at 6.00% | Estimated Monthly Savings |

|---|---|---|---|

| $250,000 | About $1,663 | About $1,499 | About $164/month |

| $400,000 | About $2,661 | About $2,398 | About $263/month |

| $600,000 | About $3,992 | About $3,597 | About $395/month |

These numbers show why the 1% rule became popular. A one-percentage-point drop can be large enough to notice in the monthly budget. But the table still does not answer whether refinancing is worth it, because it does not include the cost of getting the new loan.

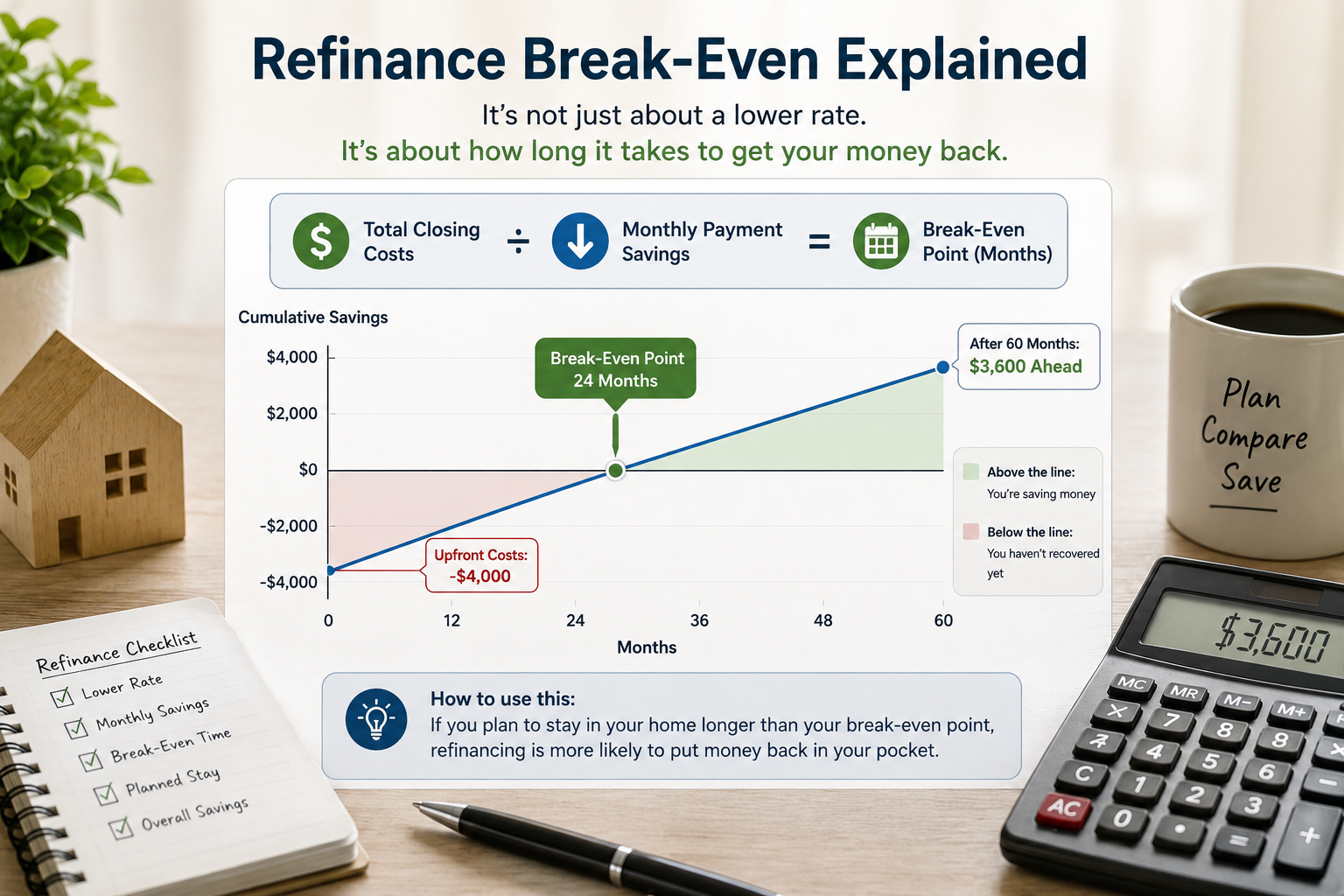

The Break-Even Point Is the First Big Test

The break-even point estimates how long it takes for monthly savings to recover the upfront cost of refinancing. The simple version is:

Break-even point = refinance closing costs ÷ monthly payment savings

For example, if refinancing saves $263 per month but costs $12,000, the simple break-even point is about 46 months, or a little under four years.

| Example Closing Costs | Monthly Savings | Simple Break-Even Point |

|---|---|---|

| $8,000 | $263/month | About 30 months |

| $12,000 | $263/month | About 46 months |

| $18,000 | $263/month | About 68 months |

| $24,000 | $263/month | About 91 months |

This is why two homeowners can see the same rate drop and make different decisions. If one person expects to stay for ten more years, a four-year break-even period may be acceptable. If another person may sell in two years, the same refinance may not have enough time to pay for itself.

Why the Simple Break-Even Formula Is Not Enough

The simple break-even formula is useful, but it can hide important details. It usually compares closing costs against monthly savings, but it may not fully account for the loan term, financed closing costs, escrow changes, points, mortgage insurance, or the total interest paid over time.

A refinance can look attractive if you only compare this month’s payment against next month’s payment. But a lower monthly payment can happen for two reasons:

- The rate is lower, which can be a real savings.

- The loan term is stretched back out, which can reduce the payment but keep you paying longer.

That second part is the trap. If you are 8 years into a 30-year mortgage and refinance into a new 30-year mortgage, you may be moving from 22 years remaining back to 30 years. Your monthly payment may fall, but your total years of debt can increase.

When a 1% Rate Drop Is More Likely to Be Worth Refinancing

A refinance after a one-percentage-point rate drop is more likely to make sense when several of the following are true.

- You have a large remaining loan balance. The same rate drop usually saves more dollars per month on a larger mortgage.

- You plan to keep the home beyond the break-even point. The longer you stay after break-even, the more time you have to benefit.

- Your closing costs are reasonable. Lower fees shorten the break-even period.

- You are not adding unnecessary years to the loan. A new 20-year or 25-year term may sometimes preserve more of your progress than restarting a full 30-year term.

- Your credit, income, and equity have improved. Better borrower profile can help you qualify for stronger pricing.

- You can remove mortgage insurance. If refinancing also removes PMI or changes an FHA loan into a conventional loan, the monthly savings may be larger than the rate change alone.

When a 1% Rate Drop May Still Not Be Worth It

A lower rate is not automatically a good deal. Refinancing may be a poor fit if the new loan solves one problem but creates another.

Be cautious if:

- You are likely to sell before the refinance breaks even.

- You already have a low balance, so the monthly savings are modest.

- The lender is charging high points or fees to show a lower rate.

- You are resetting a loan that is already many years into repayment.

- You are rolling closing costs into the new loan without comparing the true financed cost.

- The lower payment is only lower because the new loan has a much longer term.

- You are planning to refinance again soon if rates drop further.

This does not mean you should never refinance in those situations. It means the 1% rule is not enough. You need to compare the full cost of staying with your current loan against the full cost of taking the new loan.

Should You Wait for Rates to Drop Even More?

This is one of the hardest parts of refinancing. If rates have already dropped by 1 percentage point, it is natural to wonder whether you should wait for another drop.

Waiting can help if rates fall further, but it can also backfire if rates rise again or if lender fees change. The decision depends on how much you would save today, how long the break-even period is, and whether you would be comfortable refinancing again later.

One practical way to think about it:

- If the numbers are clearly strong today, waiting may not be necessary.

- If the break-even period is already too long, waiting may be reasonable.

- If you expect to move soon, waiting or skipping the refinance may be safer.

- If a lender offers a very low-fee refinance, the break-even point may be short enough to act sooner.

You cannot control future mortgage rates. You can control whether today’s offer makes sense under conservative assumptions.

Compare the Right Numbers Before You Decide

Before you say yes to a refinance, compare more than the headline interest rate. A strong refinance analysis should look at the full picture.

- Current monthly principal and interest. This is the mortgage payment before taxes, insurance, HOA, and other housing costs.

- New monthly principal and interest. This shows the payment on the proposed new loan.

- Total monthly housing payment. Taxes, insurance, HOA dues, and mortgage insurance may not fall just because the interest rate falls.

- Closing costs paid out of pocket. These affect your cash today.

- Closing costs rolled into the loan. These affect your loan balance and long-term cost.

- Points. Paying points can lower the rate, but you need to know how long it takes to recover that upfront cost.

- Remaining loan cost. This is what your current mortgage is expected to cost if you keep it.

- New loan cost. This is what the refinance is expected to cost over your selected time horizon.

- Planned-stay comparison. The best answer may be different if you expect to stay 3 years versus 15 years.

Run the Refinance Numbers Before You Apply

Home Decision Lab’s Refinance Analyzer helps you compare your current loan against a new loan offer, including monthly payment difference, closing costs, break-even point, remaining loan cost, new loan cost, cash-out if applicable, and total home cost over your planned stay.

Do Not Ignore Loan Estimates

Once you are serious enough to compare lenders, ask for Loan Estimates for the same type of refinance. A lower rate from one lender may come with higher fees, more points, or different terms. A slightly higher rate from another lender may have lower upfront costs and a shorter break-even point.

Review the interest rate, APR, loan amount, closing costs, estimated cash to close, points, lender credits, and whether the rate is locked. Also check whether taxes, insurance, mortgage insurance, or escrow items are changing.

If one offer looks much better than the others, ask why. Make sure you are comparing the same loan type, same term, same lock period, and same assumptions.

What About a “No-Cost” Refinance?

A “no-cost” refinance can sound attractive because it may reduce or eliminate the cash you need at closing. But no-cost usually does not mean free.

In many cases, the lender either charges a higher interest rate, rolls costs into the new loan balance, or gives lender credits in exchange for pricing that may cost more over time. This can still be useful if you need a short break-even period or want to preserve cash, but you should compare it against a lower-rate option with upfront costs.

The right question is not whether the refinance is called “no-cost.” The right question is: Which option leaves you better off over the time you expect to keep the loan?

What If You Want Cash Out?

A cash-out refinance is a different decision from a simple rate-and-term refinance. If you take cash out, you are increasing the loan balance. That can make the monthly payment, total interest, and long-term risk very different.

A 1% lower rate may not be enough to justify a cash-out refinance if the new balance is much larger. The cash you receive may be useful for home improvements, debt consolidation, or investing in a business, but the money is still borrowed against your home.

Before using a cash-out refinance, compare:

- The new loan balance versus your current loan balance.

- The cash received at closing.

- The new monthly payment.

- The total cost of borrowing over your planned stay.

- The risk of converting unsecured debt into debt secured by your home.

A Simple Decision Framework

If rates drop by 1 percentage point, use this framework before deciding.

Step 1: Estimate the Monthly Savings

Compare your current principal and interest payment against the proposed new principal and interest payment. Then compare the full housing payment, including taxes, insurance, HOA, and mortgage insurance.

Step 2: Calculate the Break-Even Point

Divide total refinance costs by monthly savings. If the break-even point is longer than your likely time in the home, refinancing may not make sense.

Step 3: Compare the Loan Term

Look at how many years are left on your current mortgage. Then compare that with the new loan term. A lower monthly payment may be less impressive if it adds many years of payments.

Step 4: Compare Out-of-Pocket Cost vs Financed Cost

Paying costs out of pocket affects cash today. Rolling costs into the loan affects the balance and future interest. Neither is automatically wrong, but they should be compared honestly.

Step 5: Stress-Test Your Plan

Ask what happens if you sell earlier than expected, rates drop again, your income changes, or your insurance and property taxes rise. A good refinance should still make sense under realistic conditions.

So, Should You Refinance If Rates Drop by 1%?

Maybe. A one-percentage-point rate drop is often enough to investigate refinancing, especially if your loan balance is large and you plan to stay in the home for several more years.

But it is not an automatic yes. The refinance must pass the cost test, the break-even test, the loan-term test, and the planned-stay test.

A good refinance usually does at least one of these things:

- Reduces your monthly payment enough to improve cash flow.

- Reduces your total interest cost over the period you expect to keep the loan.

- Shortens your loan term without creating an unaffordable payment.

- Removes expensive mortgage insurance.

- Improves stability by moving from an adjustable rate to a fixed rate.

- Supports a larger financial goal without taking on unreasonable risk.

If the refinance only makes the monthly payment look better while increasing your long-term cost, it may not be the right move.

Frequently Asked Questions

Is it always worth refinancing if rates drop by 1%?

No. A 1 percentage point drop is a useful reason to check the numbers, but it does not guarantee that refinancing is worth it. Closing costs, loan term, points, equity, credit profile, and your expected time in the home all matter.

How do I know my refinance break-even point?

A simple estimate is total refinance costs divided by monthly savings. For example, $12,000 in costs divided by $300 in monthly savings equals a 40-month break-even point. A more complete analysis should also consider loan term, financed costs, points, taxes, insurance, and total interest.

Should I refinance into another 30-year mortgage?

It depends. A new 30-year mortgage may create the lowest monthly payment, but it can also extend the time you are in debt. If you have already paid your current mortgage for several years, compare a 20-year, 25-year, or custom-term option if available.

What if rates drop again after I refinance?

You may be able to refinance again later, but each refinance can involve new costs. If today’s refinance has a long break-even period, refinancing again too soon could reduce or erase the benefit.

Does refinancing lower property taxes or homeowners insurance?

Usually no. Refinancing can change your mortgage principal and interest payment, but property taxes and homeowners insurance are separate housing costs. Your total monthly payment may not fall as much as the mortgage payment if taxes or insurance are rising.

Final Thoughts

A 1 percentage point rate drop can be a strong signal to review your mortgage. It can create meaningful monthly savings, especially on larger loan balances.

But the smart move is to compare, not guess. Look at your current loan, the new rate, the new term, closing costs, points, mortgage insurance, cash needed at closing, and how long you realistically expect to keep the home.

If the numbers work over your planned stay, refinancing may improve your cash flow and reduce your loan cost. If the numbers do not work yet, waiting may be the better decision.

Want to compare your current mortgage against a lower-rate offer? Use our Refinance Analyzer to estimate monthly savings, break-even point, closing cost impact, and long-term loan cost.

Sources

Educational only. This is not financial, legal, tax, mortgage, investment, or real estate advice.