5 Situations Where Refinancing Actually Loses You Money

A lower mortgage payment does not always mean a better refinance. Learn five common situations where refinancing can cost more than it saves, including short break-even timelines, term resets, high closing costs, discount points, and risky cash-out decisions.

Refinancing can be a smart move when it lowers your total cost, improves your cash flow, shortens your payoff timeline, or helps you replace a risky loan with a more stable one. But refinancing can also quietly lose you money, even when the new monthly payment looks better.

The mistake many homeowners make is comparing only the interest rate or only the monthly payment. A refinance is a full financial trade: you may pay closing costs, restart your loan term, finance fees into the balance, buy points, change mortgage insurance, or turn home equity into new debt. The right question is not simply, “Is the new rate lower?” The better question is: Will this new loan improve my financial position over the time I expect to keep the home?

Key Takeaways

- A lower monthly payment is not always a win. A refinance can reduce cash flow pressure while increasing the total amount you pay over time.

- Break-even timing matters. If you sell, move, or refinance again before you recover your closing costs, the refinance may be a net loss.

- Restarting the mortgage clock can be expensive. A new 30-year loan after years of payments may add years of interest, even at a lower rate.

- “No-cost” does not mean free. Closing costs may be rolled into the loan balance or exchanged for a higher interest rate.

- Cash-out refinancing can be risky. It may convert home equity into new debt and can stretch short-term expenses across decades.

First: What Does “Loses You Money” Mean?

A refinance loses you money when the total financial benefit is smaller than the total cost. That can happen in several ways. You might pay thousands in closing costs and move before you recover them. You might lower your payment by extending the loan, but pay more interest over the full timeline. You might buy discount points and then sell too soon. Or you might take cash out, increase your loan balance, and reduce your home equity without a clear payoff plan.

This does not mean refinancing is bad. It means the decision should be measured across multiple angles:

- Monthly payment change

- Closing costs and cash needed at closing

- Break-even point

- Remaining loan cost versus new loan cost

- How long you expect to stay in the home

- Whether your new loan term is longer, shorter, or the same

- Whether you are taking cash out or rolling costs into the loan

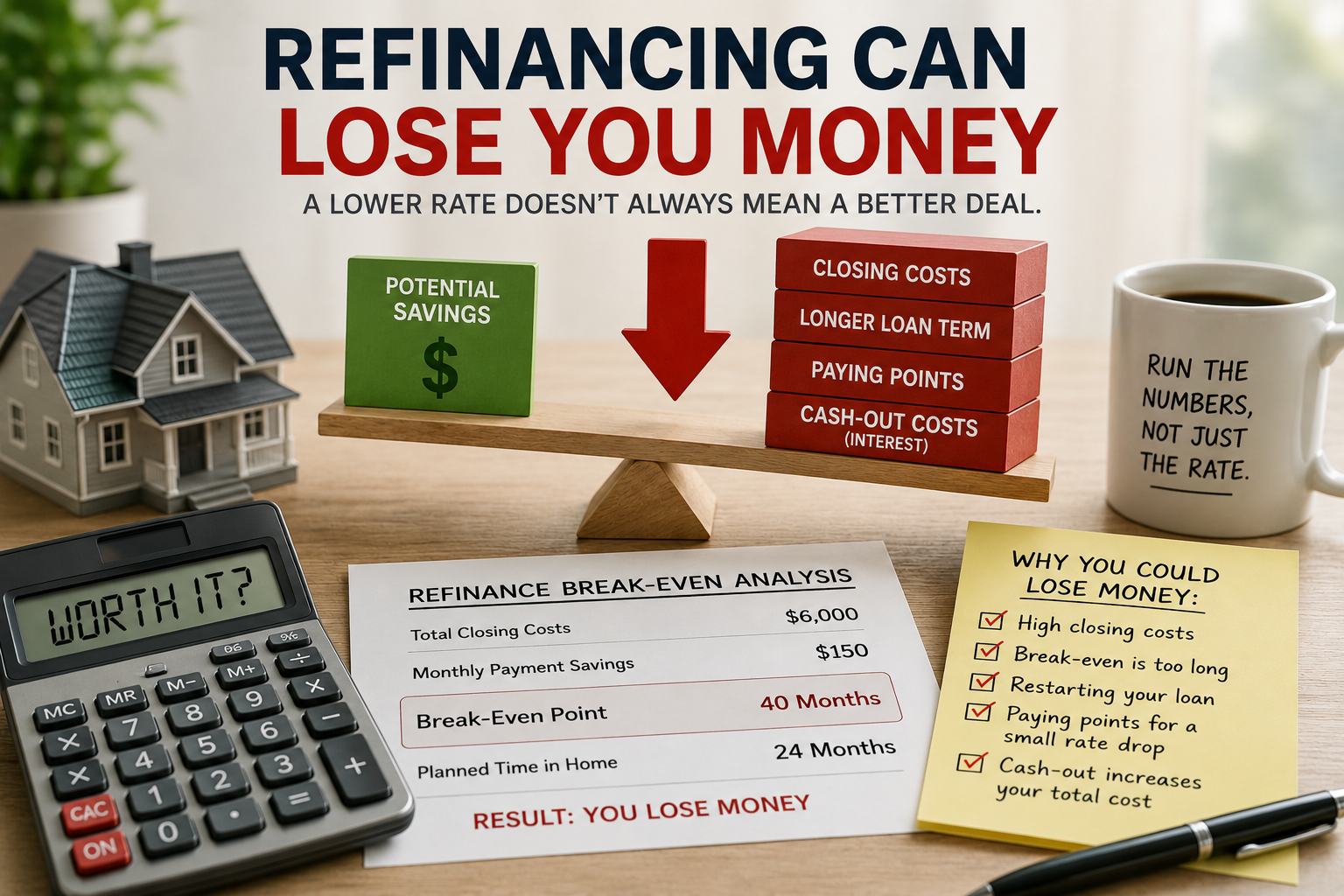

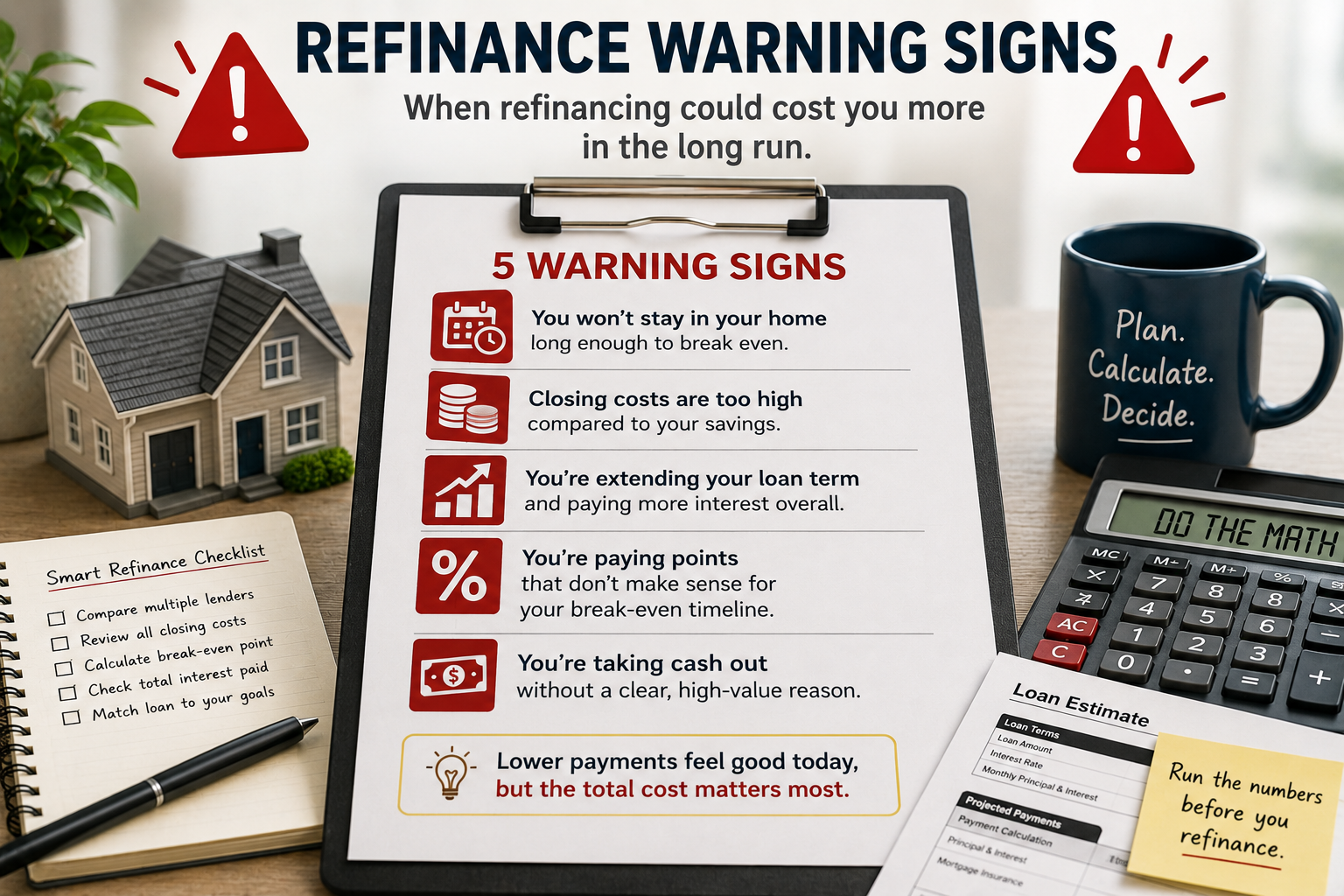

Situation 1: You Will Move Before the Break-Even Point

The break-even point is the amount of time it takes for your monthly savings to recover the upfront cost of refinancing. A simple version of the calculation is:

Break-even point = refinance closing costs ÷ monthly savings

For example, if refinancing costs $7,200 and saves you $200 per month, your simple break-even point is 36 months. If you sell the home in 18 months, you may save $3,600 in monthly payments but spend $7,200 to get those savings. That would leave you roughly $3,600 behind before considering any other changes.

This situation is especially common when:

- You are likely to relocate for work.

- You are planning to upgrade or downsize soon.

- You may sell because of family, school, or lifestyle changes.

- You expect rates may drop again and you may refinance again soon.

The practical rule: if your break-even point is longer than your realistic stay in the home, refinancing may lose money even if the new rate is lower.

Situation 2: You Restart a 30-Year Loan After Already Paying for Years

A refinance replaces your current mortgage with a new loan. If you have already paid down your mortgage for many years, starting over with a new 30-year term can make the monthly payment look attractive while adding years of payments.

Here is a simplified example:

| Scenario | Remaining Balance | Rate | Term | Approx. Monthly P&I | Approx. Total Future P&I |

|---|---|---|---|---|---|

| Current loan | $400,000 | 6.50% | 20 years left | $2,982 | $715,750 |

| New refinance | $408,000 | 5.75% | 30 years | $2,381 | $857,152 |

In this example, the refinance lowers the monthly principal and interest payment by about $601. That sounds good. But because the new loan runs for 30 years and includes $8,000 of rolled-in costs, the borrower could pay about $141,000 more over the full loan timeline if they make only the scheduled payments.

The homeowner may still choose the refinance if they need cash-flow relief. But they should understand the trade: the monthly payment improves, while the long-term cost may get worse.

Situation 3: The Rate Drop Is Too Small Compared With the Fees

A lower rate does not automatically mean the refinance works. The savings must be large enough to justify the closing costs, lender fees, title fees, appraisal costs, recording fees, and other charges.

This is why a 0.25% or 0.50% rate drop may not be enough for some homeowners. It depends on the loan balance, costs, term, credit profile, and how long the homeowner expects to keep the loan. A smaller loan balance usually creates smaller monthly savings, which means it can take longer to recover the upfront costs.

Be careful when the offer sounds like this:

- “Your payment will drop by $100 per month.”

- “You do not need to bring cash to closing.”

- “You can roll everything into the loan.”

- “The rate is lower, so it is obviously worth it.”

The missing question is: How much does the refinance cost, and how long will it take to recover that cost? A refinance with $5,000 in costs and $100 in monthly savings takes about 50 months to break even. That may be fine if you will keep the home for 10 years. It may be a loss if you sell in two or three years.

Situation 4: You Buy Points but Do Not Keep the Loan Long Enough

Discount points are upfront fees paid to reduce the interest rate. They can make sense when you keep the loan long enough for the lower monthly payment to repay the cost of the points. They can lose money when you sell or refinance before that point-based break-even period.

For example, imagine you pay $4,000 in points to lower your monthly payment by $80. The simple break-even period is 50 months. If you refinance again in two years, you received about $1,920 in monthly savings but paid $4,000 for it. That would be a poor trade.

Points can also make loan comparisons confusing. One lender may advertise a lower rate, but only because the offer includes more upfront points. Another lender may show a slightly higher rate with lower upfront costs. That is why homeowners should compare Loan Estimates side by side, not just compare the headline interest rate.

Situation 5: You Use Cash-Out Refinancing Without Fixing the Underlying Problem

A cash-out refinance replaces your current mortgage with a larger loan and gives you some of the difference in cash. This can be useful for certain goals, such as necessary home repairs, debt consolidation, or a carefully planned investment. But it can also become expensive if it turns home equity into long-term debt without improving your financial position.

Cash-out refinancing can lose money when:

- You use the cash for short-lived expenses but repay it over 30 years.

- You pay off credit cards but continue building new credit card balances.

- You increase your loan balance and monthly payment without a stable income plan.

- You give up a low existing mortgage rate to access cash at a higher blended cost.

- You reduce your home equity and leave yourself less flexibility if home values fall.

The dangerous part is that cash-out refinancing can make a financial problem feel solved temporarily. The credit card balance may disappear, the bank account may look healthier, and the monthly payments may seem manageable. But if the refinance only moves debt from one place to another, the household may end up with less equity, a larger mortgage, and the same spending pattern that created the problem.

Quick Comparison: When Refinancing May Lose Money

| Situation | Why It Can Lose Money | What to Check First |

|---|---|---|

| You move before break-even | You pay closing costs but do not stay long enough to recover them. | Break-even point compared with expected move date. |

| You restart the mortgage clock | The payment drops, but the total number of payments increases. | Remaining loan cost versus new loan cost. |

| The rate drop is too small | Monthly savings may not be enough to justify lender and closing fees. | Total closing costs and monthly savings. |

| You buy too many points | Upfront points may not pay for themselves before you sell or refinance again. | Point break-even timeline. |

| You take cash out without a plan | You may increase debt, reduce equity, and stretch short-term costs over decades. | New loan balance, payment, equity, and debt payoff plan. |

Want to See Whether a Refinance Helps or Hurts?

Home Decision Lab’s refinance tools can help you compare your current loan against a new loan, including closing costs, monthly payment change, break-even point, remaining loan cost, new loan cost, cash-out received, and planned-stay impact.

Questions to Ask Before You Refinance

Before signing a refinance offer, ask these questions:

- How much are the total closing costs?

- Am I paying those costs upfront, rolling them into the loan, or accepting a higher rate?

- What is my break-even point?

- How long do I realistically expect to keep this home?

- How many years are left on my current mortgage?

- Am I extending my payoff timeline?

- Will I pay more or less over my planned stay period?

- Will I pay more or less over the full loan timeline?

- Am I taking cash out? If yes, what exactly will the cash be used for?

- Could I reach the same goal with extra principal payments, a HELOC, a home equity loan, or simply waiting?

When Refinancing Can Still Be Worth It

Refinancing is not automatically bad. It can be valuable when the numbers and life situation line up. A refinance may be worth considering if it clearly lowers your total interest cost, reduces financial stress without creating a long-term cost problem, removes a risky adjustable-rate feature, eliminates mortgage insurance, shortens your loan term, or funds a high-value home improvement with a responsible repayment plan.

The key is to evaluate the refinance from both sides: cash flow today and net financial impact over time. Sometimes a household intentionally chooses a higher long-term cost because it needs monthly relief now. That is not always wrong, but it should be a conscious decision, not a surprise hidden inside the new loan.

Frequently Asked Questions

Can refinancing lose money even if my interest rate goes down?

Yes. A lower rate can still lose money if closing costs are too high, you move before the break-even point, you restart a longer loan term, or you buy points that do not pay for themselves.

What is the simplest way to know if refinancing is worth it?

Start with the break-even point, then compare total cost over the time you expect to keep the home. The simple break-even formula is refinance costs divided by monthly savings, but you should also compare the remaining loan cost, new loan cost, and planned-stay impact.

Is a no-cost refinance a bad idea?

Not always, but it is not truly free. The lender may charge a higher interest rate, roll costs into the loan balance, or structure the loan so the costs are paid indirectly. A no-cost refinance can work for a short-term strategy, but you should compare the full cost against a regular refinance.

Can buying mortgage points lose money?

Yes. Points can lose money if you sell, refinance again, or pay off the loan before the monthly savings recover the upfront cost of the points.

Is cash-out refinancing always risky?

Cash-out refinancing is not always bad, but it deserves extra caution. You are increasing or extending debt secured by your home. It may be reasonable for a planned investment or necessary expense, but risky for short-term spending or debt payoff without a plan to prevent the same debt from returning.

Final Thoughts

Refinancing should make your financial life better, not just make one monthly payment look smaller. The best refinance decisions compare costs, timing, interest, equity, loan term, and life plans together.

If the new loan saves money within your realistic stay period, improves your stability, and does not create a larger hidden cost, it may be worth exploring. If the savings are small, the closing costs are high, the break-even period is too long, or the refinance simply turns home equity into new debt, waiting may be the smarter move.

Before you apply, use our Refinance Analyzer to compare your current mortgage with a potential new loan, or reach out through our contact page.

Sources

Educational only. This is not financial, legal, tax, mortgage, investment, or real estate advice.